Options API for backtesting

Backtest options ideasagainst captured market snapshots.

Use historical option-chain captures, IV/HV regime fields, signals, scanner candidates, and underlying OHLCV context to test rules before they become live workflows.

History

Chains

captured contracts and expirations

Signals

Rules

test scanner and strategy filters

Context

Regime

IV, HV, price, and liquidity

Designed for repeatable research

Backtesting needs clean historical inputs. OptionChainIQ focuses on captured market snapshots you can query and join with strategy rules.

Build symbol and date loops around normalized endpoint responses.

Compare strategy rules across volatility regimes and expirations.

Feed results into notebooks, dashboards, or scheduled reports.

Use the visual dashboard to inspect outliers and examples.

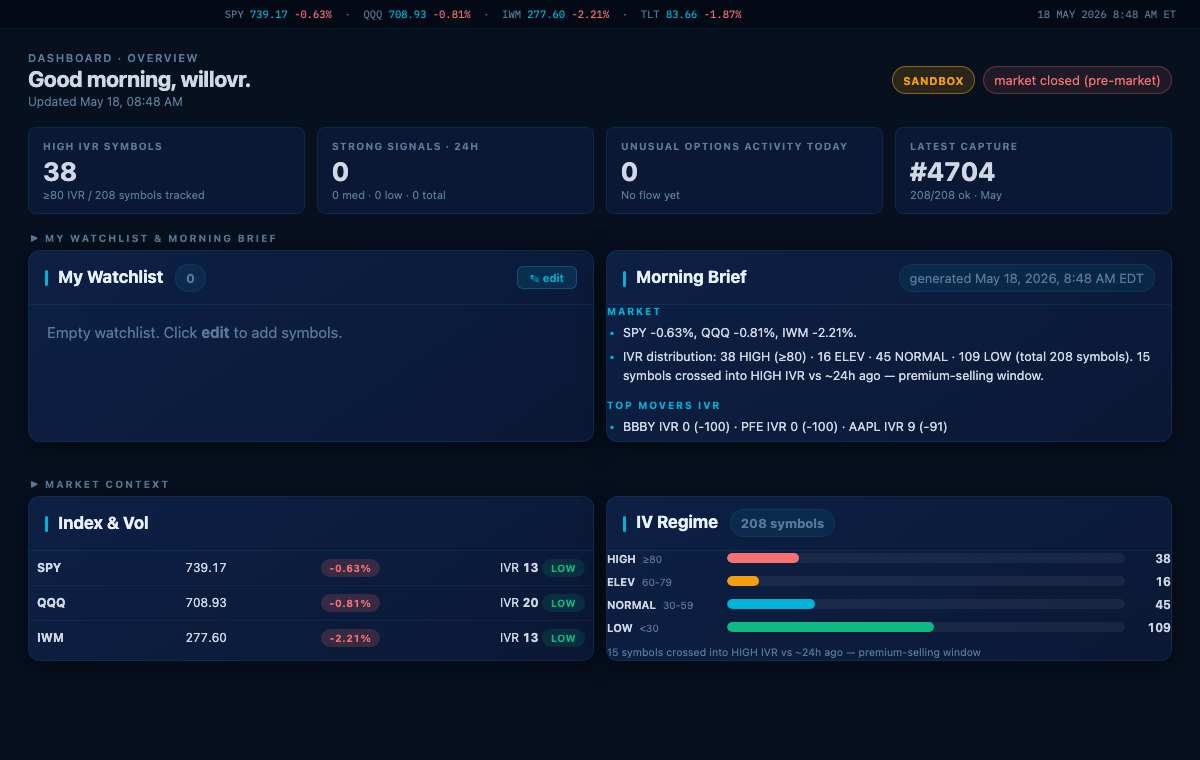

Overview: market state, latest captures, signals, and context for research workflows.

Sample response

Backtesting Snapshots JSON

GET /v1/research/snapshots?symbol=AAPL&from=2026-05-01&to=2026-05-15

{

"symbol" : "AAPL" ,

"snapshots" : [

{

"date" : "2026-05-15" ,

"underlying_close" : 211.26 ,

"contracts" : 1842 ,

"atm_iv" : 23.84 ,

"iv_rank" : 41.2 ,

"hv_20d" : 20.4 ,

"signal_count" : 7 ,

"trade_idea_count" : 12

}

]

}

Research Test rule changes Compare how filters behave across different market snapshots and volatility states.

Automation Run scheduled notebooks Pull repeatable JSON data into Python, REST Client, or internal analysis jobs.

Review Inspect examples visually Use the dashboard to understand why a strategy candidate passed or failed a filter.